Newsletter Summer 2018

Maximize Your Productivity & Profitability with a PEO

Work on your business instead of in your business. A PEO (Professional Employer Organization) partners with companies to provide comprehensive HR outsourcing, employee benefits, compliance and payroll.

Generally with PEOs, your employees have access to a wider variety of benefits at a cheaper cost than your company could get on its own. By pooling all its client companies together, a PEO has greater buying power when it comes to negotiating rates with benefits providers. Such benefits include health, vision, dental, flexible spending accounts, retirement plans, life insurance and more.

PEOs process payroll for your employees. They manage the regular compensation of employees along with payroll record maintenance and management, payroll compliance, online pay stubs and W-2s, payroll management reports and PTO accruals.

A PEO also helps with HR. They help to manage your liabilities as an employer, providing employee handbooks, new hire on-boarding, termination assistance, employee relations support, liability management training and more.

Worry about government compliance? You won’t have to with a PEO. It’s their job to constantly monitor changes to state and federal labor laws that could affect your business, as well as advise you on what actions you need to take to comply.

A PEO takes care of workers’ compensation coverage and claim resolution. Specialists can guide you through the process surrounding work-related injuries, including monitoring claims and assisting injured workers’ return to work.

PEOs are great for small and mid-sized companies. By outsourcing some of the more tedious day to day office tasks, they let owners focus on managing core business functions while saving significant time and money.

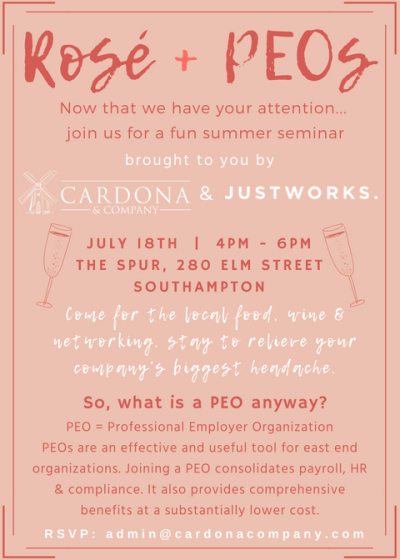

Interested in learning more? Join us as we partner with Justworks, one of the many PEOs we work with, next month on July 18th at The Spur in Southampton. We will be hosting a free summer seminar from 4:00pm – 6:00pm. We will be happy to answer any questions you may have and help you decide if switching to a PEO is right for your company.

If you would like to attend please email admin@cardonacompany.com

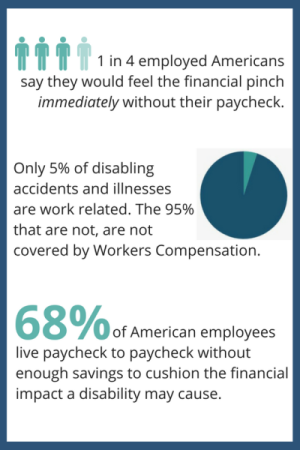

A Growing Need for Disability Insurance

May was Disability Insurance Awareness Month. Disabilities can occur at any time, so it’s important to protect your income with Disability Insurance.

What’s your biggest asset? Your paycheck. Disability Insurance helps protect a portion of your income if you become mentally or physically unable to work. Disability Insurance would provide you with payments that would help cover living expenses such as rent, car payments, childcare and more.

Disability Insurance could also help you avoid using your retirements savings to cover income gaps. Policies can be customized to suit your individual needs. For example, you may be able to choose to add a rider to your policy which allows your coverage to grow as your income grows.

Not sure how much Disability Insurance you need? Click here to view a Disability Insurance Calculator to find out. While this is not a comprehensive assessment, it will give you a general idea of how much coverage you may need.

Newsworthy Headlines and Updates

IRS Announced New Changes in May Regarding HSA Contributions

In March the IRS announced that the maximum family HSA contribution limit had been lowered to $6,850 for 2018. Last Thursday, the IRS announced that taxpayers may treat $6,900 as the maximum annual family HSA contribution limitation instead of $6,850. Because so many people had already contributed the full $6,900 or set their payroll deductions for the year based on that amount, the IRS is allowing people to contribute $6,900 for 2018.

If you contributed $6,900 at the beginning of the year, and then lowered your contribution in response to the initial change in March, you will generally have the following options, subject to tax filing deadlines:

- You may repay that distribution to your HSA up to the limit of $6,900; OR

- retain the funds as a tax-free HSA distribution

- This distribution would not need to be included in gross income or subject to excise tax unless the excess contribution is attributable to an employer or payroll deduction

- If the excess contribution is attributable to an employer or payroll deduction and was not subject to income tax, then the amount will need to be included in gross income unless the taxpayer can show there is a corresponding qualified medical expense.

Learn more about HSAs here.

Paid Family Leave Payroll Deduction Update

Employers do not need to cap the weekly employee payroll deduction for Paid Family Leave at .126% of the New York State Average Weekly Wage (NYSAWW) (approximately $1.65 per week in 2018.) Instead, employers may deduct .126% of an employee’s weekly wage until the employee hits the annual cap of $85.56, which is .126% of the annualized NYSAWW.

This applies to employees with a weekly earning greater than the current NYSAWW ($1,305.92).

This update will better position employers to collect the full Paid Family Leave premium from each employee. Certain employees will now meet their annual maximum PFL deduction of $85.56 before the year is over.

You can estimate weekly deductions by using the PFL weekly payroll deduction calculator here.

If you have any questions about how this will affect your business you should contact for your payroll company.

To learn more about the Paid Family Leave program visit our blog.

PCORI Fees Due by July 31, 2018

For clients with an HRA attached to your health insurance:

Under the Affordable Care Act (ACA) a fund was created to assist in clinical effectiveness research. To aid in the financial support for this endeavor certain health insurance carriers and health plan sponsors are required to pay fees based on the average number of lives covered by welfare benefits plans. These fees are referred to as either Patient-Centered Outcome Research Institute (PCORI) or Clinical Effectiveness Research (CER) fees.

PCORI fees are required to be submitted by July 31st for your Health Reimbursement Arrangement (HRA). Fees are reported and paid once per year with the submission of Form 720 (Quarterly Federal Excise Tax Return). Indexed each year, the fee amount is determined by the value of national health expenditures. The fee phases out and will not apply to plan years ending after September 30, 2019. To determine your PCORI fee, multiply the applicable fee by the average number of annual participants. The applicable fee is based on the end of your HRA plan year:

Plans ending between January 1, 2017 and September 30, 2017 have a fee of $2.26. If your HRA ended between October 1, 2017 and December 31, 2017 your fee is $2.39

More information about the PCORI fee can be found on the IRS website here. Feel free to contact our office if you have further questions.

What do our clients have to say?

News & Events

Winter Newsletter 2018

A special thank you! As 2018 comes to an end, we would like to thank all of our clients for your...

Read moreMissed Open Enrollment? Options for Coverage for 2019

Open Enrollment ended on December 15th. Most people need to wait until next year's Open Enrollment...

Read moreDNA Testing Kits and Life Insurance

DNA Testing Kits, such as 23andMe, have become a popular item. They are tests that allow...

Read moreCrowdfunding to Pay for Medical Costs

It's no surprise that healthcare costs are on the rise in America. After all, healthcare in the US...

Read moreStay Healthy This Holiday Travel Season

Do you have plans to travel this holiday season? We'd like to help keep you healthy and away from...

Read moreHow to Open an HSA: What You Need to Know About Health Savings Accounts

An HSA is a Health Savings Account where you can put aside pre-tax dollars to pay for qualifying...

Read more