What Factors Affect Your Life Insurance Rating?

Thinking about buying life insurance? Have you ever wondered what goes into getting a life insurance policy? The process is pretty straight forward. You meet with an insurance agent, fill out an application, take a medical exam (sometimes), and wait for an approval. The life insurance company reviews your application and if approved, gives you a rating. The rating determines how much you will pay for your policy. The better the rating, the less you pay for the policy.

So what goes into determining your rating? Many factors affect how you are rated; some you can control, and some you can’t. Read on to see what affects your rating and how:

Age

So you can’t control your age, but it is one of the first things an insurance company looks at when determining your rating. The younger you are the more likely you are to get a better insurance rating. Since there is less risk of death, younger individuals receive lower rates. That’s why it’s smart to purchase life insurance while you are young.

Sex

The one is pretty simple. Women generally live longer than men, so women pay lower rates.

Current Health

Life insurance companies are essentially placing a bet on how long you will live. So it’s no surprise they’ll want to take a look at your health. Most insurance companies require you to take a basic medical exam before they give you a policy. The exam will gather information such as your weight, height, cholesterol and blood pressure. They can also test for nicotine use. If you are in good health, you will most likely get a good rating.

Besides the exam, many insurance companies will often request medical records going back five years. If something comes up in those records, they may request records going back even further. If you are young, healthy and get good results

If you have a health condition such as asthma or diabetes, you may get a lower rating. However, life insurance companies will want to know if you have the condition under control or not. Say you have diabetes, for example. An insurance company is likely to give you a higher rating if you have you take medication regularly and have your symptoms under control. This is why it is important to disclose all of your health information to your insurance agent so that he or she can communicate with the insurance company on your behalf.

Smoking and Drinking

Smokers automatically get a lower rating when applying for life insurance. Because smoking has so many proven health risks, people who smoke get a smokers rating which is automatically more expensive—a lot more expensive that a non-smoker. Heavy alcohol consumption can also affect your health and result in a lower rating for life insurance.

Family history

While your own health history also plays a role in your life insurance rating, so does your family history. These are one of the factors that you cannot control but insurance companies are interested in. If a parent passed away at an early age due to a hereditary disease, this could affect how insurance companies rate you.

Weight

Being overweight comes with more risk of serious health problems. If you are overweight or obese, you may end up paying more for coverage.

Job

What you do for a living can affect your life insurance rating. Occupations that require you to perform dangerous duties can put you at a higher risk of accidental death and will result in higher premiums. Jobs like airline pilot or firefighter would have a higher risk of death.

Hobbies

Certain activities such as race car driving and skydiving will play a factor in your life insurance underwriting process. High-risk hobbies can increase insurance costs.

Driving

Your driving habits don’t just affect your auto insurance. If you have multiple driving violations you are considered to be at a higher risk for accidents and therefore may have to pay high life insurance rates.

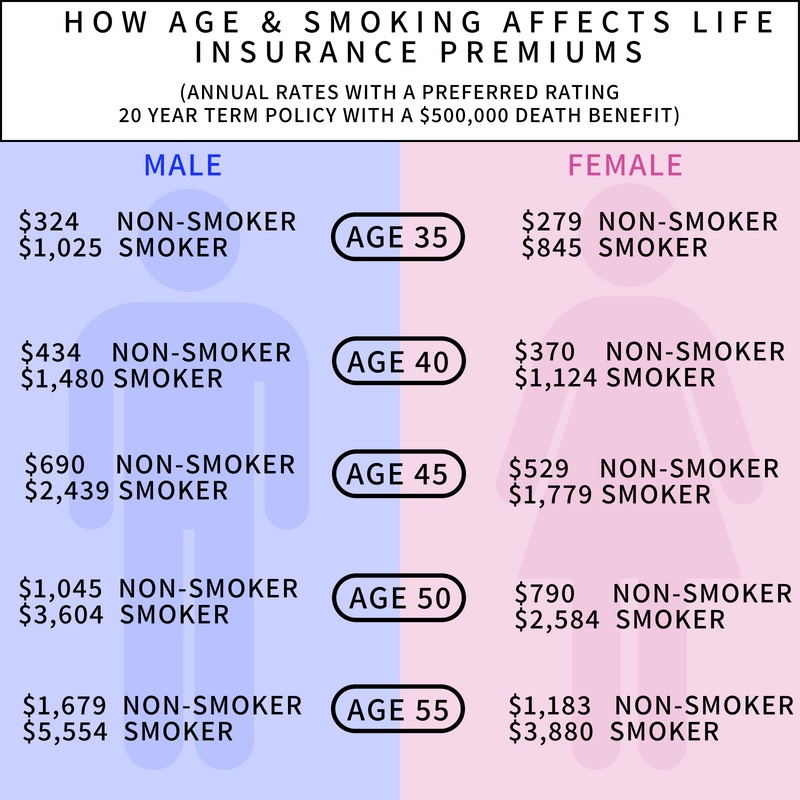

The chart below shows how gender, age and smoking can affect your life insurance premium.

What do our clients have to say?

News & Events

Winter Newsletter 2018

A special thank you! As 2018 comes to an end, we would like to thank all of our clients for your...

Read moreMissed Open Enrollment? Options for Coverage for 2019

Open Enrollment ended on December 15th. Most people need to wait until next year's Open Enrollment...

Read moreDNA Testing Kits and Life Insurance

DNA Testing Kits, such as 23andMe, have become a popular item. They are tests that allow...

Read moreCrowdfunding to Pay for Medical Costs

It's no surprise that healthcare costs are on the rise in America. After all, healthcare in the US...

Read moreStay Healthy This Holiday Travel Season

Do you have plans to travel this holiday season? We'd like to help keep you healthy and away from...

Read moreHow to Open an HSA: What You Need to Know About Health Savings Accounts

An HSA is a Health Savings Account where you can put aside pre-tax dollars to pay for qualifying...

Read more