Be Prepared for Open Enrollment

It’s that time of year when many company’s health insurance plans are renewing, which means that you may have the option of changing your health insurance plan, or enrolling in a plan for the first time.

While not all companies give their employees different health insurance options, a lot do, and it’s important to know what plans are being offered, how to choose the plan that is best for you, and what questions to ask during open enrollment.

Open Enrollment is the period in which you can make changes to your health insurance plan, add beneficiaries, or opt into (or out of) coverage.

The most important thing to know is how to choose a health insurance plan. We like to tell our clients that we can absolutely tell you what plan is best for you… in year from now. The truth is, you can’t actually predict what type of plan you will need (unless you have ongoing medical issues/costs or anticipate any surgeries in the upcoming year.)

So there are two questions we suggest you ask yourself in order to pick the right plan:

- What network is best for you? Are there certain doctors that you absolutely need to see? If so, then you should look at what plans/networks your doctors are on.

- Do you want to pay more in monthly premiums, or more when you go to the doctor? You can pay for a cheaper plan, but that means you will likely pay more out of pocket costs when visiting the doctor and purchasing prescriptions. So if you don’t go to the doctor very often, you may want to choose a plan with a lower premium, just expect to pay more when you see your doctor.

Once you have those two questions answered, you will have a good idea of which type of plan you should enroll in.

Some employers pay for a portion of your premiums. Ask your employer if they contribute anything to your health insurance plan so you know what your monthly cost will be. It is helpful to know how much you are spending each month so you can budget for the year.

It’s also important to decide if you need vision and dental coverage. Not all employees offer this, but if they do, you should ask what services the plans cover and what doctors are in the network. You should approach vision and dental plans the same way you approach your health insurance plan.

You can also find out if the health insurance plans offered have any type of gym reimbursement. Some plans provide a reimbursement for gym memberships as well as other health programs/classes to encourage healthy living.

Health insurance plans can seem confusing if you don’t understand the health insurance lingo. Some of the most common phrases that can confused people are:

premium: the amount you pay each month for your health insurance coverage

deductible: the amount you pay for healthcare services your plan covers before your health insurance plan begins to pay. [for example, if you have a $2,000 deductible, your plan won’t pay anything until you pay the $2,000 deductible for covered healthcare services]

maximum out of pocket (MOOP): the most you pay during a policy period before your health insurance plan begins to pay 100% of the allowed amount. [after you spend this amount on deductibles, co-pays, and co-insurance, your health plan pays 100% of the costs of covered benefits. this does not include your monthly premium]

co-payment (co-pay): an amount you pay as your share of the cost for a medical service or item [like $50 for a doctor’s office visit]

co-insurance: your share of the cost for a covered healthcare service, which is calculated as a percentage [like 30%] of the allowed amount for the service. you pay co-insurance plus any deductibles you owe. [for example: if the health plan’s allowed amount of an office visit is$100 and you have met your deductible, your co-insurance payment of 30% would be $30. your insurance pays the rest of the allowed amount]

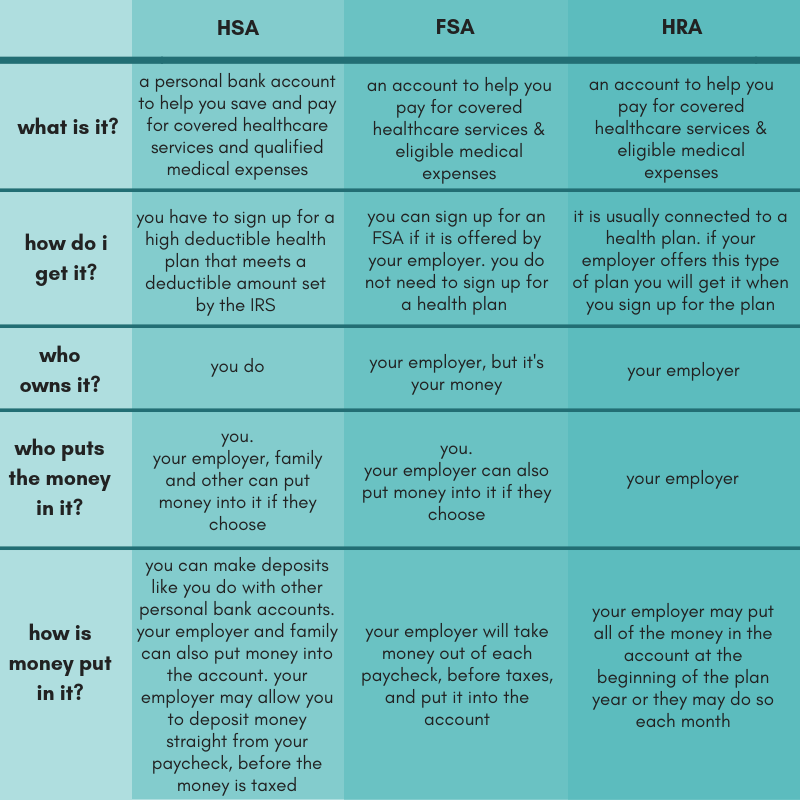

Ask your employer about HRAs, FSAs and HSAs. These are three different types of accounts that can be used to pay for certain medical expenses while saving on taxes. You can also read our blog that breaks down the differences between the three accounts.

Some employers also offer disability insurance or life insurance policies during open enrollment. Depending on your finances, you may want to consider purchasing this ancillary benefits. They can sometimes be cheaper than trying to buy the policies on your own, but it’s also important to consider if these policies are necessary or the right fit for you. It would be wise to ask if these types of insurance policies are portable, or if you can take them with you if you leave your job. If not, it is worth speaking to a life insurance agent to see what type of life and disability insurance policies are available to you.

Open enrollment can be overwhelming and confusing. There is a lot of information and a lot of questions to ask, but if you are prepared and do your health insurance homework, you will be well-prepared to choose a plan that fits your needs and your budget.

What do our clients have to say?

News & Events

Winter Newsletter 2018

A special thank you! As 2018 comes to an end, we would like to thank all of our clients for your...

Read moreMissed Open Enrollment? Options for Coverage for 2019

Open Enrollment ended on December 15th. Most people need to wait until next year's Open Enrollment...

Read moreDNA Testing Kits and Life Insurance

DNA Testing Kits, such as 23andMe, have become a popular item. They are tests that allow...

Read moreCrowdfunding to Pay for Medical Costs

It's no surprise that healthcare costs are on the rise in America. After all, healthcare in the US...

Read moreStay Healthy This Holiday Travel Season

Do you have plans to travel this holiday season? We'd like to help keep you healthy and away from...

Read moreHow to Open an HSA: What You Need to Know About Health Savings Accounts

An HSA is a Health Savings Account where you can put aside pre-tax dollars to pay for qualifying...

Read more