The Growing Need for Disability Insurance

According to data from the American Council of Life Insurers, 51.3 million households in the United States are without disability insurance other than the basic coverage available through Social Security. At least 51 million Americans are without adequate income protection.

This is a problem. One in four of today’s 20-year olds will be out of work for at least a year because of a disabling condition before they reach 67, the normal age of retirement. Further, nearly 6% of working Americans will experience some type of short term disability (6 months or less) due to illness, injury or pregnancy on average ever year.

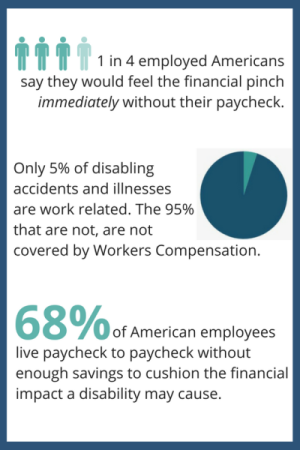

With no income protection in place, a lot of Americans experience severe financial difficulty. Seven in ten working Americans admit they would feel the financial pinch in a month or less without their paycheck.

Many Americans may think they can rely on Workers’ Compensation or Social Security Disability Insurance if they become disabled or injured an unable to work. This is a common misconception that could cause serious problems.

Workers’ Compensation only covers time away from work if the injury or illness was directly work-related. In 2016, only 1% of American workers missed work because of an occupational illness or injury.

There are also several problems with relying on Social Security Disability Insurance. The average benefit as of January 2018 was $1,197 per month, which equates to $14,364 annually. This is barely above the poverty guideline of $12,140 for a one-person household and below the poverty guideline of $16,640 for a two-person household.

It can take anywhere from 3-5 months to get an initial decision on SSDI benefits after you apply. In 2017, the backlog of appeals cases was more than 1 million, with an associated processing time averaging more than 18 months. Many Americans don’t have enough money saved up to cover expenses for 3-5 months.

Besides a small monetary benefit, and a long waiting period, only 34% of SSDI claimants actually had their applications approved. Just 23% of the approvals were at the initial stage and the remainder only after a reconsideration or appeals process.

Relying on Workers’ Compensation and SSDI is a risky bet. Since most disabling injuries and illnesses are not caused at work, Workers’ Comp isn’t a reliable source of income to fall back on. The SSDI process is lengthy, approval isn’t guaranteed, and the payout is not a lot.

Your income is your biggest asset. Disability Insurance helps protect a portion of your income if you become mentally or physically unable to work. Disability Insurance would provide you with payments that would help cover living expenses such as rent, car payments, childcare and more. If you are too sick or too hurt to work, Disability Insurance could help you avoid using your retirement savings to cover income gaps. It is possible to customize your Disability Insurance policy to suit your individual needs. For example, you may be able to choose to add a rider to your policy which allows your coverage to grow as your income grows.

Disability Insurance is a smart investment. It’s something you would rather have and not need, than need and not have.

What do our clients have to say?

News & Events

Winter Newsletter 2018

A special thank you! As 2018 comes to an end, we would like to thank all of our clients for your...

Read moreMissed Open Enrollment? Options for Coverage for 2019

Open Enrollment ended on December 15th. Most people need to wait until next year's Open Enrollment...

Read moreDNA Testing Kits and Life Insurance

DNA Testing Kits, such as 23andMe, have become a popular item. They are tests that allow...

Read moreCrowdfunding to Pay for Medical Costs

It's no surprise that healthcare costs are on the rise in America. After all, healthcare in the US...

Read moreStay Healthy This Holiday Travel Season

Do you have plans to travel this holiday season? We'd like to help keep you healthy and away from...

Read moreHow to Open an HSA: What You Need to Know About Health Savings Accounts

An HSA is a Health Savings Account where you can put aside pre-tax dollars to pay for qualifying...

Read more